Private Equity Has Redefined Market Realities: it’s Wartime.

PE has rewritten the rules of American business. AI is poised to accelerate this shift. Are you ready?

By Jim Jonassen, JJA Founder

As executive headhunters, each partner on the JJA team builds and nurtures relationships across an ecosystem we call Growth & Innovation. Most of the businesses in our ecosystem rely on investment capital in the form of venture and/or private equity to fuel growth and value creation. We have a unique vantage point, given that we spend our days in conversations with company leaders, private equity sponsors, venture investors and advisors/service providers who also serve that ecosystem. In parallel, we’re interviewing talented leadership candidates about their career direction and for the searches we are filling. These discussions have revealed a megatrend that you may already be aware of and an insight that we’ll share in hopes we can discuss it further with you. Here goes:

- The growth, increasing dominance and influence of Private Equity are undeniable.

- This upheaval has changed the rules of engagement across markets, every business in our ecosystem, and much of the economy at large.

- The “peacetime” of the last 15 years has yielded to *wartime.

- The players who embrace the new reality and adapt quickly will survive, and maybe even thrive.

- Artificial Intelligence will pour gasoline onto this fire.

* I use the term wartime based on the framework a16z cofounder Ben Horowitz applied in his New York Times bestseller, The Hard Thing About Hard Things. Ben described peacetime in business as an environment where markets are growing, there is abundance, and leaders can focus on very long-term big, hairy, audacious goals. Wartime is when a business is faced with threats in real-time from competitors, the macroeconomic climate, major market shifts or black swans.

Is your career, your company or your portfolio armed and ready for wartime?

The genesis of this article was a lunch conversation with my pal, Dave Young, a longtime Partner at Cooley, LLP and the de facto mayor of Silicon Beach. Dave has been the legal counsel of choice in over 2,000 formations, financings and exits for startups across the innovation economy (fka Tech). He shared with me that nearly half of today’s VC-backed startup exits are acquisitions by PE. That’s up from about 5% a decade ago—a 10X increase!

“Nearly half of today’s VC-backed startup exits are acquisitions by PE – up from just 5% a decade ago. That’s a 10X increase!”

Dave Young, Partner, Cooley

Dave enlightened me, “For the first half of my 30-year career, I think that I only had one or two deals involving the sale of a VC-backed company to a PE acquirer (most sold to strategics while a few actually IPO’d). The landscape really has changed, and this has been a huge benefit to the growth company ecosystem and flywheel – especially with companies waiting longer than ever to go public.”

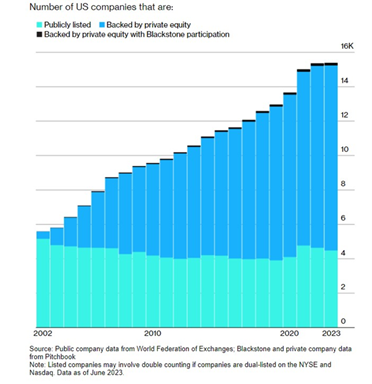

The ascendency of private equity in five charts – cue the hockey stick.

The modern private equity industry surfaced just 35 years ago. Known back then as buyout firms, key early PE players included Warburg Pincus, the Bass family, Kohlberg Kravis Roberts (KKR), Forstmann Little and individual “raiders” like T. Boone Pickens, who famously attempted to take over Gulf Oil in 1983.

The rules of this game were forever changed when KKR won its $25 billion bid to acquire RJR Nabisco in 1988.

That deal was twice the size of Chevron’s Gulf purchase for $13.4 billion just four years earlier. In today’s dollars, the RJR Nabisco transaction would be an $800 billion deal. RJR put KKR (and PE) on the map. The mega-deal was immortalized in the 1989 bestselling book Barbarians at the Gate: The Fall of RJR Nabisco.

Over the past 20 years, the number of PE-backed and owned companies in the US has increased from 1,900 to 11,200. That’s nearly a sixfold increase, and the trend shows no signs of slowing.

Another eye-opener is that the number of publicly traded US companies has dropped from around 8,000 in 1997 to just 4,300 today. No, it’s not that America somehow has 40% fewer companies now than it did 30 years ago. But a much higher percentage are now choosing (or being forced) to remain private.

Meanwhile, Statista reports that the domestic PE market is expected to reach $460 billion in 2024. And by 2027, it’s expected to top $765 billion, with a compound annual growth rate (CAGR) of 11%. In terms of Assets Under Management, the numbers are already measured in the trillions.

Skadden Arps summed things up well recently: “In the last decade, private capital assets under management (AUM) of all types have shown sustained growth, more than doubling from less than $10 trillion globally in 2012 to more than $24 trillion by the end of 2022, driven by strong returns for investors, according to an August 21, 2023, EY report.”

But wait, there’s more: a handful of very recognizable PE fund managers (think Apollo Global Management, Ares, Blackstone and KKR) now control $1 trillion of private lending. Each started out in PE and distressed-debt trading before expanding into credit.

Private lending now accounts for more capital than the entire U.S. banking system.

Finally, in terms of capital available to deploy, or “dry powder,” Bain’s 2024 PE Outlook reports that “Buyout funds alone are sitting on a record $1.2 trillion in dry powder.”

PE works on a very straightforward business model:

- Buy/invest in an asset at the right entry price

- Hold it typically for 3-5 years (shorter = better)

- Create Value: Grow margins and EBITDA <full stop>

- Sell for a multiple of greatly enhanced EBITDA

- Return (ideally 4X) to stakeholders (LPs, GPs and Shareholders)

So, if PE is now (or is quickly becoming) the dominant Funder, Lender and Buyer – isn’t it time to get with their program? Today, that means adopting a wartime mindset.

How is wartime different from peacetime?

A few of Ben Horowitz keen insights on the differences include:

- The peacetime CEO “knows what to do with a big advantage.” The wartime CEO is “paranoid.”

- The peacetime CEO “aims to expand the market.” The wartime CEO “aims to win the market.”

- The peacetime CEO “builds scalable, high volume recruiting machines.” The wartime CEO does that but also “builds HR organizations that can execute layoffs.”

The most recent peacetime period began just after the GFC (circa 2009). It accelerated through the post-pandemic stimulus but then quickly went airborne off a cliff in early 2022 (leaving no skid marks at the edge). This rising tide lifted (almost) all boats. It was characterized by:

- Unlimited Capital Chasing Risk: On-demand equity capital from series seed to series G and beyond, driven by limited partners plowing capital into alternative investment vehicles (PE, VC, Hedge Funds and more) due to near-zero yields in conventional investment categories like stocks, bonds and cash.

- ZIRP: the recession and later COVID-induced Zero Interest Rate Period where near-free credit was slathered on top of equity capital, which extended runways and enhanced the burn.

- Ever-rising valuations with unicorns being minted at a blistering pace; “Blitzscaling” companies valued as a multiple of revenue run-rate and growth. The next financing round became everybody’s primary objective.

- Liquidity: The exits were wide open; record-breaking M&A, with retail investors gobbling up everything from IPOs to ICOs to meme stocks.

The shifting macro has driven a wartime context since the innovation economy sailed off that cliff in early 2022. This new era is characterized by:

- Interest rates added 500+ basis points, with a forecast of “higher for longer.”

- Availability of credit tightened dramatically after the crash of banks like Credit Suisse and SVB.

- Bid-ask spread disparity froze the M&A market. It seems acquisition targets preferred their 2021 valuations to the “corrected” offers they’ve received since the bubble burst.

- The IPO window shut.

- Most importantly, the only real acquirers are PE sponsors. And they’re looking for a value-priced entry point.

- Financial Engineering: PE now relies increasingly on secondaries, continuation vehicles and private credit as LPs crack the whip for returns and for GPs to put their dry powder to work in new deals.

How to avoid getting “Hagened”

In his role as the new Godfather, Michael Corleone had to tell Tom Hagen, “You’re out, Tom. You’re not a wartime consigliere.” And that’s precisely what we’re seeing unfold today.

An Operating Partner at one of the world’s top PE shops recently shared that they had replaced (top-graded) over a third of their portfolio CEOs in the previous two quarters. In other words, they were Hagened. Because it’s wartime.

Wartime does not mean relentless aggression, or “moving fast and breaking things.” That’s Sonny, Michael’s doomed older brother. In peacetime, one can be a thinker or a shoot-from-the-hip leader. In wartime, both fail. Because wartime requires both access to privileged information, and a penchant for decisive swift action. It means acting fast but learning faster.

If you get nothing else from this post, understand that the days of no-brainer, formulaic decisions are over. You must be able to make the smart decision in almost every situation and make it based on synthesizing the intel you’ve collected. You must surround yourself with partners and teammates who have access to expertise, intel and “alpha” that you can leverage.

Leading effectively today means doing everything at an unprecedented pace. In wartime, the only constant is accelerating change. So how do you adapt? Stay relevant? Thrive? Here are some great places to start:

Elevate and recruit wartime leadership that has:

- Delivered under harsh conditions

- Made tough decisions in the face of crisis and exhibited resilience in turbulent market conditions

- Used data-driven insights to inform high-velocity decisions

- Built and maintained high-performance cultures

- Embraced speed and agility

Reevaluate business strategies and revise playbooks:

- Overreliance on peacetime frameworks and historical pattern recognition will lead to defeat

- Scrutinize your organization’s current strategy to ensure they’re aligned with the new market realities

- Establish a clear vision, including frameworks to respond quickly to market changes and opportunities

- Arm managers and teams with competitive advantages for the battles ahead

Focus on operational excellence and EBITDA.

- Emphasize relentless, efficient execution to drive growth and profitability.

- Ensure all teams are aligned, motivated and equipped for the fight

- Remove status quo from your vocabulary

Leverage the latest warfare technology (hint, that’s AI)

- Quickly develop and operationalize AI for your business – adapt as you go

- Invest in AI technologies to go on the offense, or you’ll find yourself playing defense

- Provide training for those who want it and a nice severance package for those who don’t

- Actively recruit AI-obsessed talent

- Move at AI speed

So, what now?

How you begin assessing the world around you through recalibrated optics depends on your role, the stage of your career, and, of course, where you work. Whether it’s a VC or growth equity-backed company or one that is private equity-owned (or soon will be), we suggest starting at the top and taking a hard look at company, as well as functional/departmental leadership.

Can you confidently say that you have wartime leaders who are built to survive and thrive in the New World Order? Can you count on them to handle the intense rigor, the increased scrutiny, and the inescapable imperative for relentless execution?

As an executive search firm, JJA is assessing our entire network through this wartime-based lens. We are researching, identifying and surfacing these types of leaders for our clients. We also know this isn’t a matter of choice – not if we want to maintain the sort of track record that motivates clients to partner with us in the first place. And if you are interested in hiring wartime leaders, shoot us a call.

What’s your take? As always, we’re keen to add your insights to the observations we receive every day. Feel free to reach out to me, Sam or Jason any time.

Cue the cliffhanger…

If you picture this whole wartime scenario as a wildfire, then AI is quickly becoming highly flammable fuel being air-dropped onto this blaze. If you thought the pace of “Internet time” was fast back in the 90s, then based on the dizzying progress in GenAI and LLM development over the past year, it’s safe to say you ain’t seen nothin’ yet!

In our next installment, we’ll go deep into the outsized influence of AI. Stay tuned.

####

Hey – my name may be on the byline, but the ideas I share are always the product of a team effort. JJA is on a mission to keep raising the bar in high-stakes executive search. For more insights, sign up for our free newsletter, The Executive Summary,on our LinkedIn page. Meanwhile, feel free to hit me up at any time. Always happy to talk.

And please check out our exclusive ThursdayNights.org. events. A JJA community investment, Thursday Nights has been convening leaders of the innovation economy while serving at-risk youth since 2007. We also have a lot of fun.